In my practice I am regularly asked by some clients to give my views on the direction of the Rand relative to their investments or those portions of their investments that are exposed to other geographic regions and currencies of the world. This, of course, calls for extreme caution on my part as I am led in my views by the opinions of the experts on these matters and even they can’t stick their necks out too far in terms of prediction. What they, however, do is to study the trends and various global influences on currencies in order to arrive at their respective, qualified opinions.

Paul Stewart, managing director of Plexus Asset Management has the following to say: “Ultimately the direction in which a currency trends is a function of aggregate demand and aggregate supply of the currency versus other currencies. The demand for currencies is largely affected by exports, imports, service payments, portfolio investments, domestic fixed investment, foreign fixed investment and speculation on future expectations. Based on these factors, how is the SA rand likely to perform in the foreseeable future? As a general observation, the SA rand is overwhelmingly viewed as overvalued at present and that a sharp devaluation is imminent,” says Stewart. “In fact, many respected commentators have publicly stated their view that investors should currently accumulate foreign currency exposure, in anticipation of a great unwinding of the rand’s value.”

…….“currency diversification needs to be seriously reconsidered in this new world. Non-South African exposure for diversification reasons needs to be much more carefully considered. A higher emerging market currency exposure, especially to the best quality emerging markets, should be a core part of one’s investment policy.”

In order to bring the above into context

When will the rand weaken – and against what?

A currency’s value at any point in time is the equilibrium or market clearing price at which buyers or sellers of the currency will participate in the market. Ultimately the direction in which a currency trends is a function of aggregate demand and aggregate supply of the currency versus other currencies. So says Paul Stewart, managing director of Plexus Asset Management.

“The demand for currencies is largely affected by exports, imports, service payments, portfolio investments, domestic fixed investment, foreign fixed investment and speculation on future expectations,” says Stewart.

Based on these factors, how is the SA rand likely to perform in the foreseeable future? “As a general observation, the SA rand is overwhelmingly viewed as overvalued at present and that a sharp devaluation is imminent,” says Stewart. “In fact, many respected commentators have publicly stated their view that investors should currently accumulate foreign currency exposure, in anticipation of a great unwinding of the rand’s value.

“South African investors typically think of the rand’s relative value to the US dollar, euro, British pound and perhaps the Japanese yen. They seldom consider the rand in relation to the Australian dollar, Canadian dollar, Brazilian real or Chinese yuan,” he adds.

According to Stewart, the expectation for a devaluation of the rand relative to the USA, Eurozone and UK currencies may be misplaced.

“The developed world is emerging from the global financial crisis and countries are currently debt-laden,” he says. “Exceptionally high historic debt to GDP ratios, added to high unemployment rates, imply that robust growth will not return to these regions soon.

“In fact, very accommodative monetary policy (low short-term interest rates) and aggressive fiscal policy (massive upscaling of the government balance sheet) have been the selected policy tools adopted by the authorities to engender growth and restore confidence in these economic powerhouses.”

According to Stewart the unmarked footnote to these policies’ decisions is that massive stimulus and low interest rates have a cost – they will ultimately weaken their home currencies.

“This is not something politicians will readily acknowledge in the mainstream policy announcements. A depreciating currency ultimately means the gradual erosion of the purchasing power of their citizens. But currency devaluation is a recognised and tolerable policy choice given the economic challenges that face these regions,” says Stewart.

“My conclusion is that given a secular period of poor developed market economic conditions, South Africa will look good on a relative basis to these economies for the foreseeable future. South Africa has its problems and they are well documented, but its debt levels are lower, its growth rates will be higher and its commodities will continue to command a premium price in the world of a weak US dollar,” he says.

“My view is that the rand will continue to ‘surprise’ the market in how robust it is relative to the dollar, euro and British pound. Of course this does not preclude short, sharp periods of risk aversion when the rand may experience periodic jitters – such as during September 2008 and January 2011 – only to retrace its footsteps once calm returns. I would not be at all surprised to see the rand remain at these levels, or perhaps even trend stronger against these majors, in the next three years.”

“Conversely, many emerging markets (BRICM) and commodity strong economies such as Australia and Canada do not have these extreme debt concerns coupled with slow growth.

“Emerging markets specifically have good population demographics, improving government finances, high levels of net foreign reserves and the added boost of sitting on either large commodity pools or extremely competitive labour forces – or both,” he says.

“The fundamentals and outlook for such countries in terms of their currencies are actually very good. Expect these currencies to outperform in the future.”

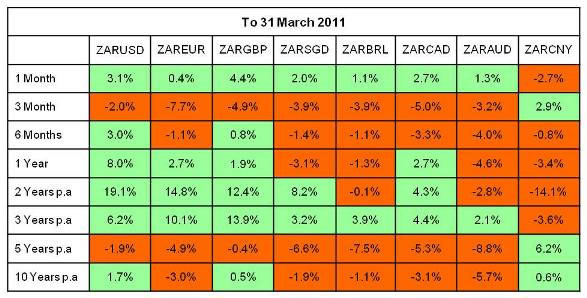

On a relative competitiveness basis, Stewart believes the South African rand could well see devaluation against this emerging market currency basket in the future as it has in the last few years (see accompanying table).

Stewart adds: “Either way, the idea of currency diversification needs to be seriously reconsidered in this new world. Non-South African exposure for diversification reasons needs to much more carefully considered. A higher emerging market currency exposure, especially to the best quality emerging markets, should be a core part of one’s investment policy.”

*Green areas denote rand appreciation, red areas denote rand depreciation

The opinion and comment in this newsletter is opinion and comment only and does not in any way constitute financial advice. Please consult a professional financial adviser for all financial decisions.